2026 - The great stall.

In a nutshell

Interest rates stuck at a high level, discouraging both buyers and sellers

The stock market is high and boosting the wealth effect, but warning signs and fear of a recession and an AI bubble are present.

During most recessions, real estate has gone up and approved to be a safe store-hold of wealth.

In our valley, we see this stalled market clearly across towns and types of real estate.

Find the latest market stats for the valley at the bottom of the article!

First off, let me apologize for having missed a few months of market updates. I’ve been working on a project (single family home renovation in Glenwood Springs) since December, and it took all my time and attention. I’ll do a publication about it soon, and show that there is still value to be found in the valley despite high rates and high prices!

So, let’s catch up with what happened in 2026 so far!

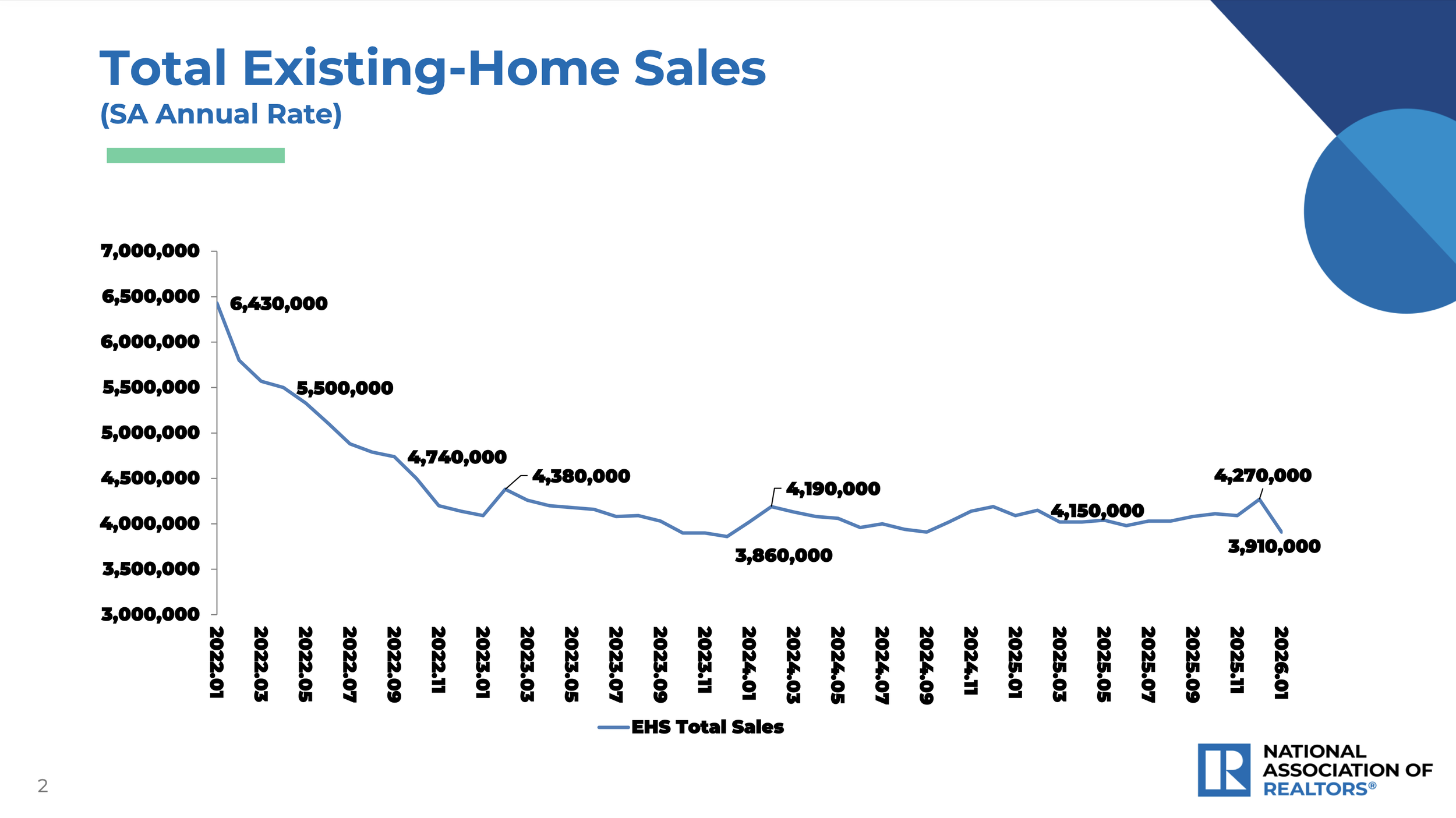

This winter both buyers and seller deserted the market. We are beating records with extremely low sales volume. Listings are down, yet with such low level of transaction, we now have almost 6 months worth of supply. Sellers are not very motivated and properties sit on the market longer. Buyers see the challenges presented by current market conditions and are hesitant to jump in. The great stall has begun.

Interest rates: why we are cornered.

Interest rates play a key role in this market. The obvious reason is that the current high level of interest rates is crushing affordability, leaving buyers on the sidelines. This means less demand, and it should produce a downward pressure on prices. But in the case of the real estate market where most sellers are also buyers, it also means less inventory. Selling your home and buying another means trading a 3% interest rate for a 6.5%. It makes people want to just stay put. That is how we explain the steady decline in inventory and sales volume. As long as interest rates stay elevated, the market will remain frozen, characterized by low volumes and high prices.

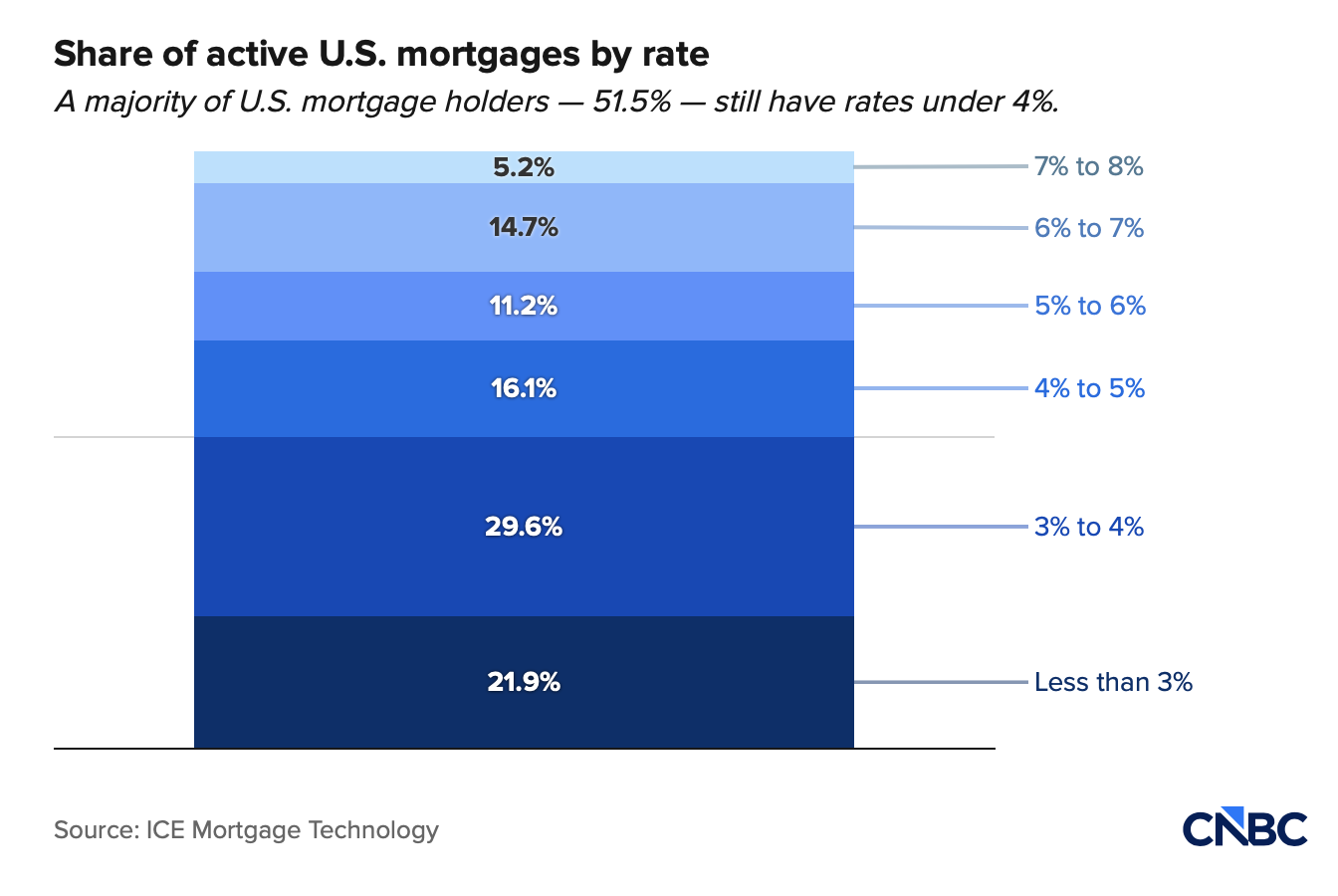

So if this market is frozen because of the difference between mortgage rates set on homes bought in the past, and the rates currently available on the market, how big is that gap and how many people are sitting on low mortgage rates?

This is rate that people currently have on their home in the US:

As you can see on the chart above, almost 68% of homeowners have a rate under 5%. Over half are a rate under 4%. Those rates were set for 30 years about 4 years ago. So there is still 25 years on the countdown until these low rate mortgage go away… Unless rates come down close to 5%.

I often compare this situation to the one created by prop 13 in California. This tax law sets a a rate at which property taxes will go up yearly for as long a the property is owned by the same person or entity, instead of reassessing the value every 2 years based on comparable sales like in our valley. In other words, it’s a huge incentive to keep your real estate, and prevents people from trading as much as they would otherwise. As we know, real estate prices in California have defied gravity for a long time, continuing to climb despite being objectively unaffordable. I often say that the 3% rates locked in after the pandemic are prop 13 for the whole country…

And if you think that things can’t get much worse than where we are, consider this: in California, nearly one out of every five property transfers last year was made through inheritance, a record for the state and double the national share”, as reported in the Wall Street Journal. The less people transact, the more unaffordable it gets.

The other factor at play here in maintaining high prices in real estate is how sticky inflation seems to be. It is my opinion that real estate will continue to be seen as a safe heaven for the rest of this cycle. Historically, being invested in real estate in inflationary time is a good thing. This cycle is characterized by sticky mid to high inflation, with government spending and deficit putting fuel on that fire. The US economy is hot and inflation gobbles people’s money faster than they can make it, and this is not the kind of environment that tends to see property values go down.

I don’t expect rates to go down, and I don’t expect values to go down this year in our area. People seem to have all the incentives they need to just keep what they have. With almost nobody wanting to sell, no matter how unattractive buying is, prices will remain high.

Why are mortgage prices so high, and what could get them down?

There is a lot of misconception about how mortgage price are set. In the world of politics, some would like to make us think that the FED chair (currently Jerome Powell) can adjust them by the push of a button. That is simply not true. In the US the mortgage rates are set on the market. Unfortunately, the pool of money used to finance mortgage rates and the US government deficit is one and the same. So as demand and supply meet on the market place, the amount of government debt directly pushes mortgage rates up. It is true that the Federal reserve can pull some levers to twist how the demand/supply play out on that market (through quantitative easing or tightening), but really if the government borrows trillions, mortgage rates will stay elevated. Unfortunately, there is no end in sight for government overspending in the US, and getting deeper into debt might be the only thing both parties can agree on.

The stock market and the fear of recession

Real estate is local, we’ll never say it enough. But it’s also influenced by its macro environment, and what’s happening nationwide and even globally. I’d describe the two main trends at the macro level by the following:

Heavy involvement of the federal government to maintain asset prices high. The current administration has had no problems getting involved in the private sector. The government took stakes into Intel, US steel, brokered deals for Tik Tok, used the economy and takes as leverage for all kinds of policy decision and implementation. And 2026 happens to be a mid-term year. So I’m fully expecting president Trump and Scott Bessent (treasury secretary) to fill up the kitchen sink, loosen monetary policy as much as the bond market will tolerate it, and create the illusion of prosperity for the year. The push to replace chair Powell and the “big beautiful bill” with its massive budget deficit are only two of the signs that point at that direction.

Asset price inflation. Not without link to the first trend described above, asset price are high and even is they generate some fear that we might be in a bubble (especially regarding the AI companies), the wealth effect is still in full force. High valuation emboldens asset owners (real estate, stocks, precious metals…) to trade and consume. Most homebuyers right now for examples are able to purchase in the current market conditions due to having sold real estate recently, at a high price also, and/or having stocks to leverage or sell in order to purchase a home.

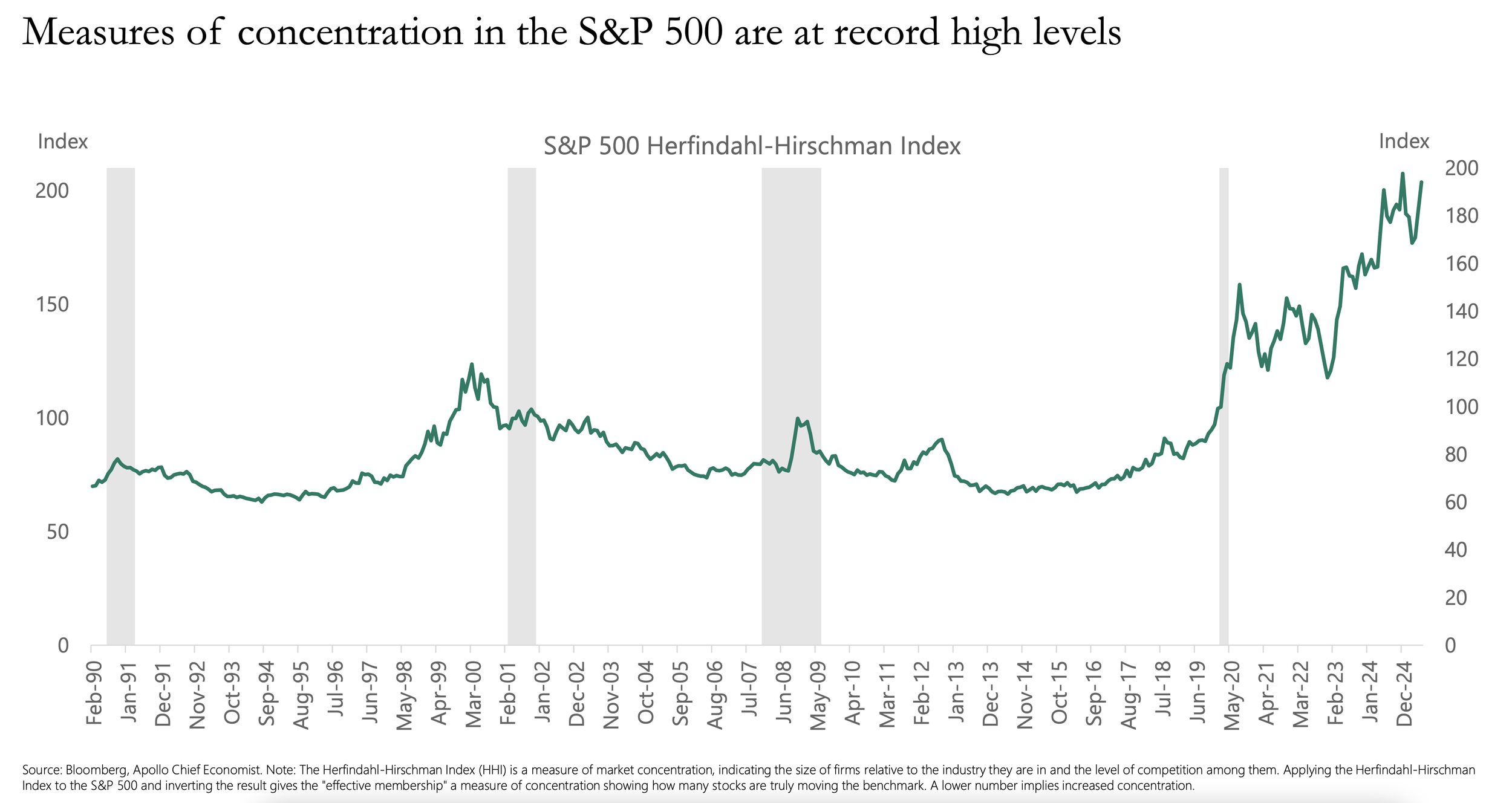

Biggest risk to the macro level: the USA is now a giant bet on AI. Reports estimate that AI-related capital expenditures surpassed the U.S. consumer as the primary driver of economic growth in the first half of 2025, accounting for 1.1% of GDP growth. JP Morgan Asset Management’s Michael Cembalest notes that “AI-related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November 2022.”

This level of concentration is rarely seen, and it’s getting us all concerned that we might be in an “AI bubble”. That being said, few things tend to be reassuring regarding that trend. The first is that most companies in the AI race (Alphabet, Meta, Apple…) are literally flush with cash and are not leveraging much to finance the capital expenditure for the AI investments.

On top of the extreme concentration of stocks in the AI domain, stock ownership is also extremely concentrated in the hands of a small group of people. According to Federal Reserve data, the top 10% of U.S. households own about 93% of all stocks and mutual fund shares. And this group of people represent an increasingly large share of the consumption (wealthy Americans, specifically the top 10% of earners, drive nearly half (around 49-50%) of all U.S. consumer spending, a historically high share, click here to read more). I see this both as a risk and a safety net. A risk because if stocks fall, these wealthy people can cut their consumption quickly and by a lot, as opposed to middle or lower income classes whose consumption is mostly made of essentials, therefore hard to trim. It’s also a safety net because as we’ve seen in 2008, asset values tend to crash when the middle or lower classes own them, and they have to foreclose or sell quickly because they don’t have the liquidity to hold these assets in a down turn. Because of this, I’d be more concerned with the price of crypto currencies, that seem to be more mainstream than stocks. Stocks have traded in the private market for long enough and most stocks are owned by people won’t won’t have to sell them quickly in a downturn.

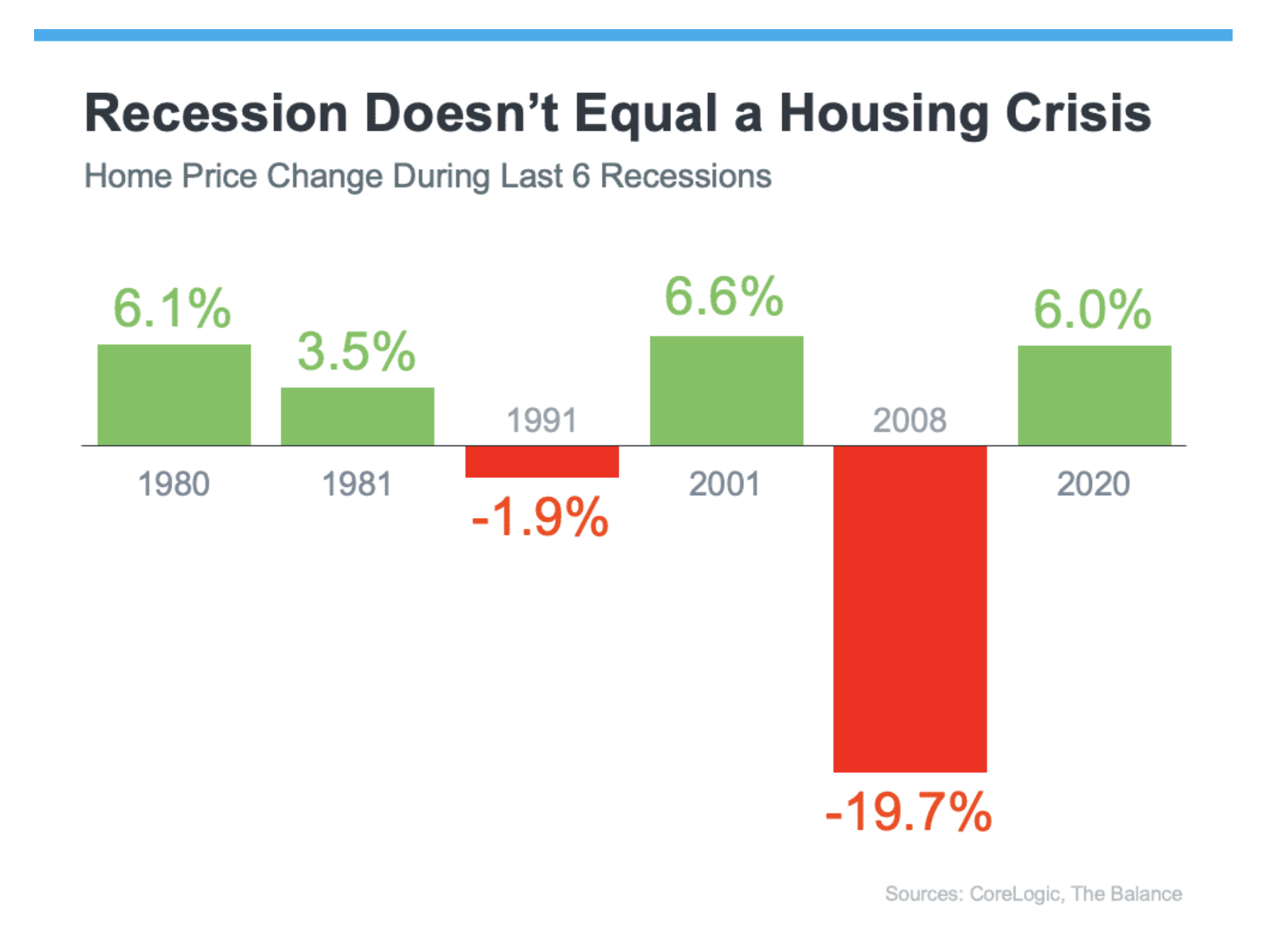

What did recessions do to property values in the past?

As you can see on the chart below, more often than not, housing is seen as a safe store-hold of wealth when a recession hits. The 2008 crisis being an anomaly, during which housing was the actual trigger for the recession. In most cases, housing actually went up during recessions, as capital flowed in ta that asset class that seem more stable in turbulent times.

You hear a lot of noise right now about an AI bubble, after the magnificent 7 decided to go to extreme CAPEX expenditure to try to win the AI race, bringing echoes of 2001. If this is the situation we are in, divesting from real estate seems to be a bad idea in the current context.

Breaking it down to the local level

Our valley was an after COVID darling and valuations are higher than anyone could have imagined before the pandemic. We’ve taken full advantage of cheap money, surging stock market valuation, and I’ll bet you, tough those numbers are hard to find, that our local inflation is worse than it is in other parts of the country. If you’ve traveled recently, you probably got a feel for it.

If our real estate seems to have followed other asset prices and can point at a higher correlation between stock market and real estate prices in our valley, I also think that it is the people creating that link, and who move their money between asset classes based on market conditions who will retreat from the stock market and into real estate if the situation is similar to 2001. If this is what we are dealing with, and the stock market corrects due to AI getting ahead of itself, we should see this frozen market getting even more stuck, with people holding on to their real estate while stocks are unattractive.

But the correlation between stocks and real estate is only a part of the story here. The reputation of our valley as a very attractive, safe and fun place to live and spend time at, as well as the physical constraint to building more homes are long term trends that shrug any kind of short term market trends. These factors amplify the lock in effect of the low interest rates set after COVID in the formation of the low inventory and sales volume that is the biggest driver of this market.

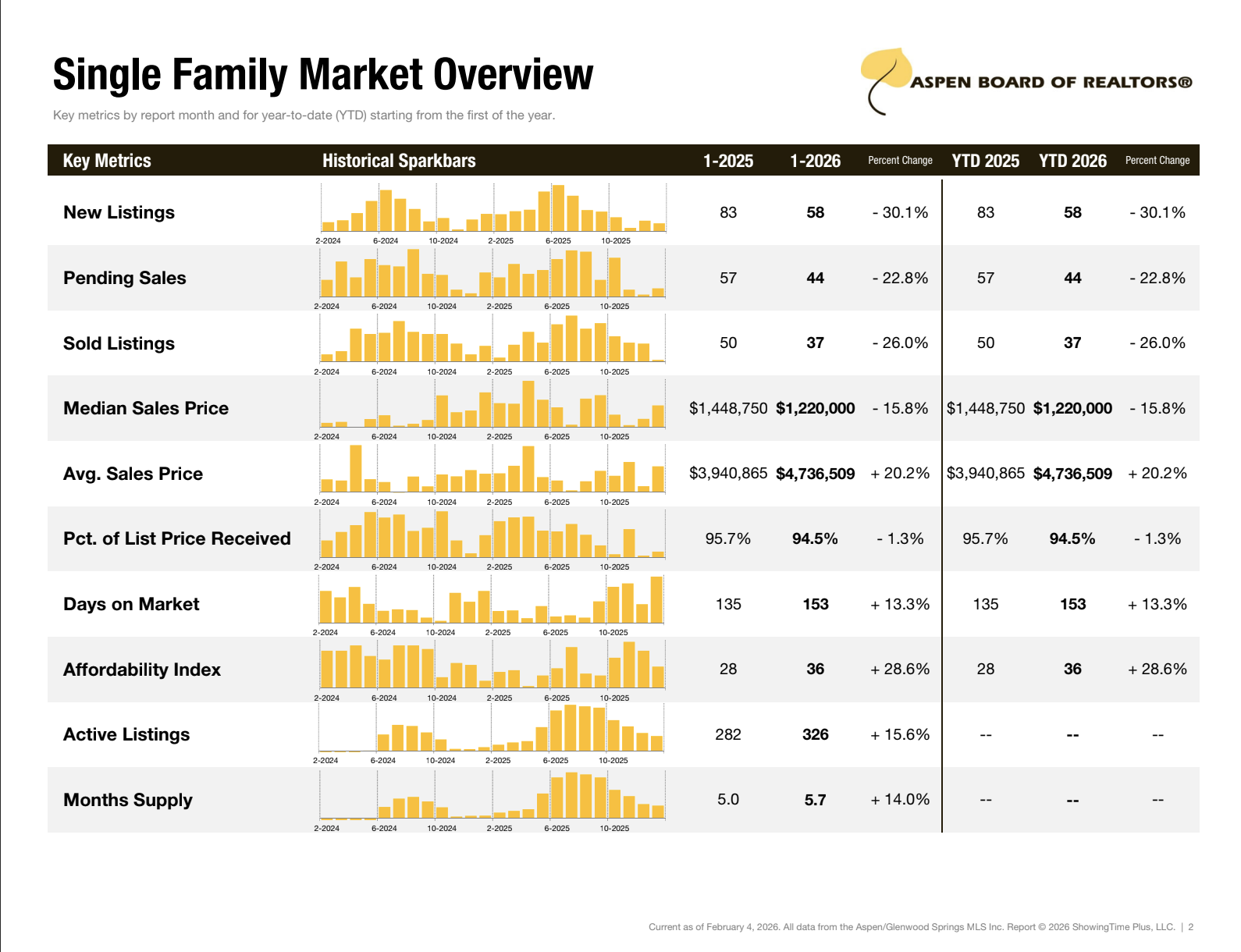

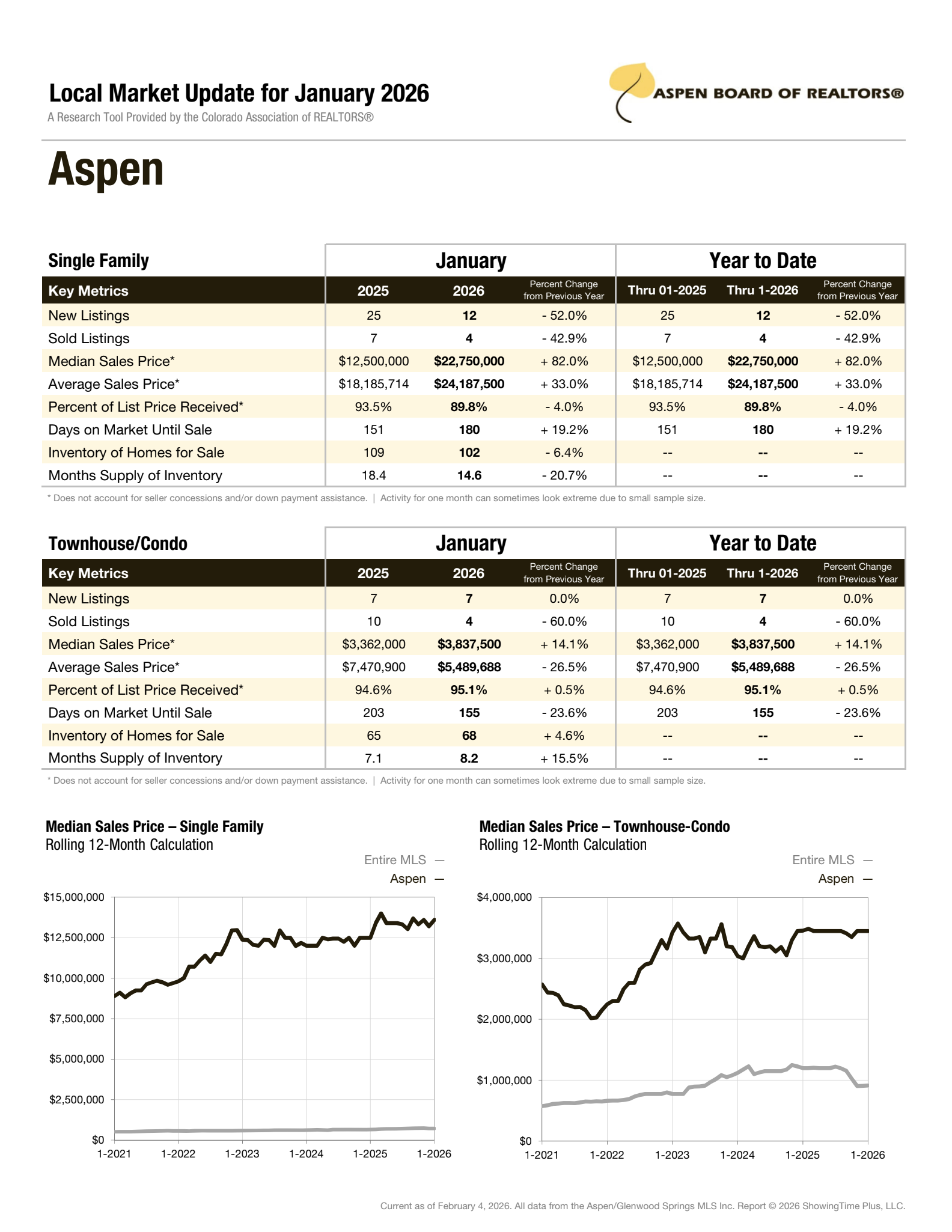

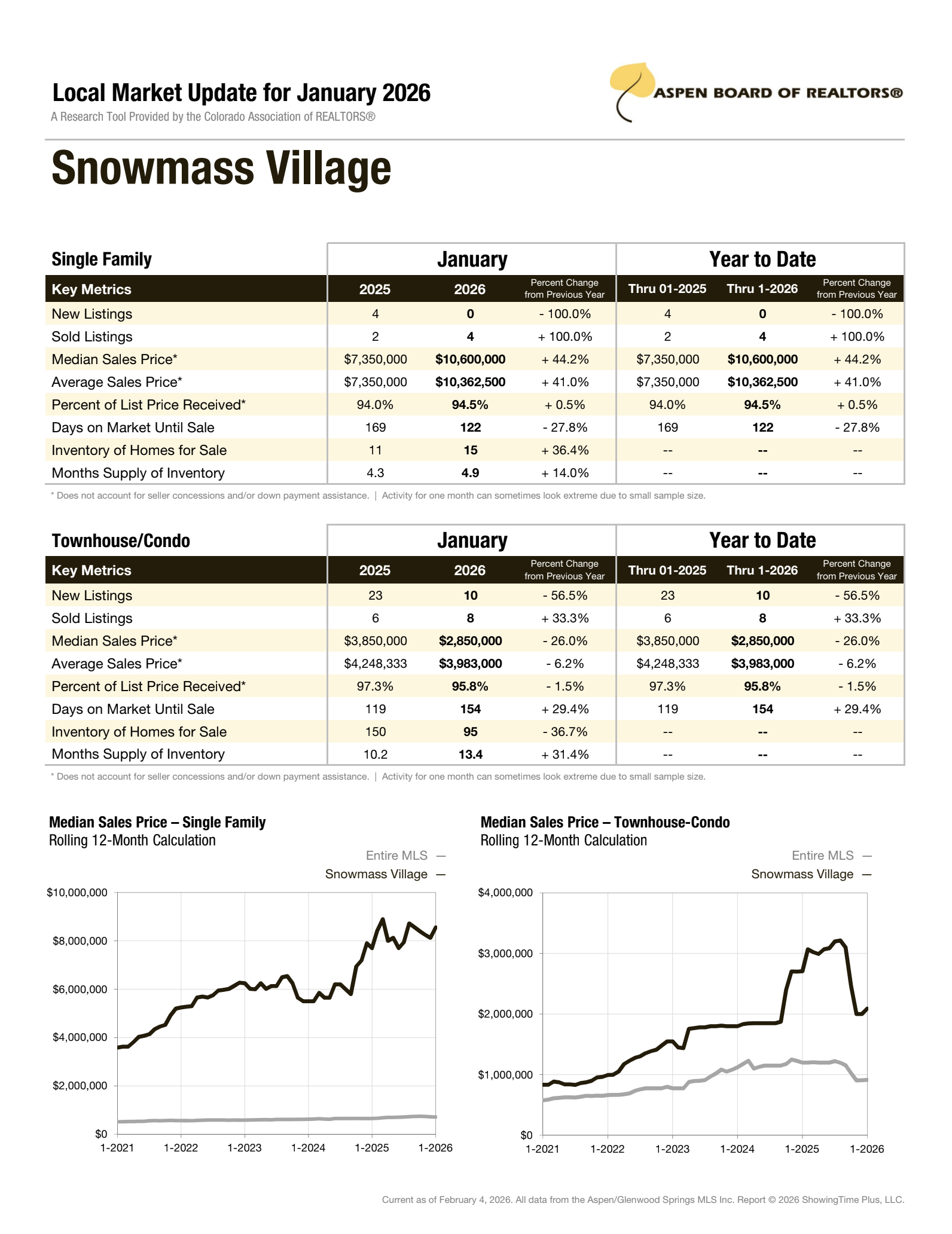

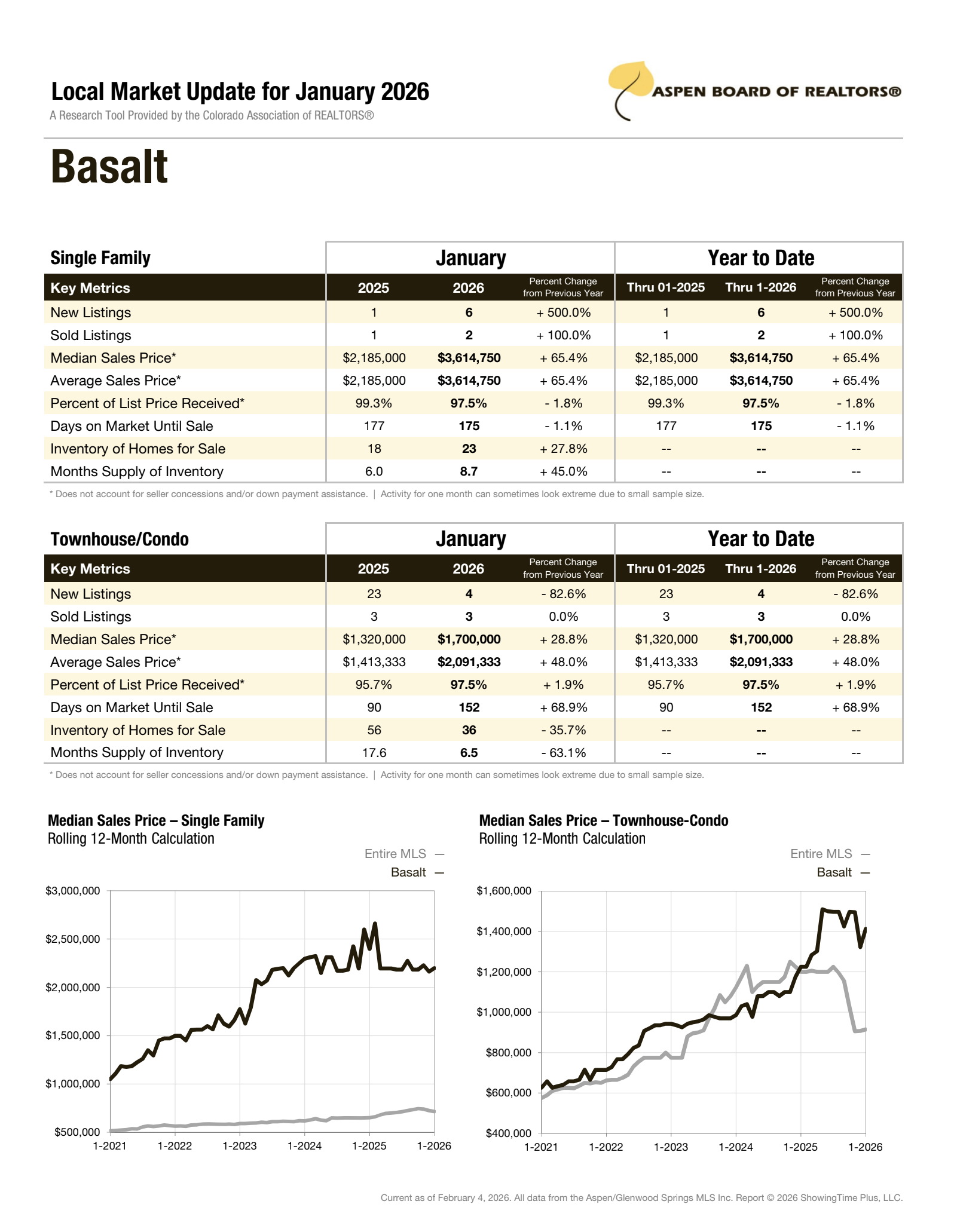

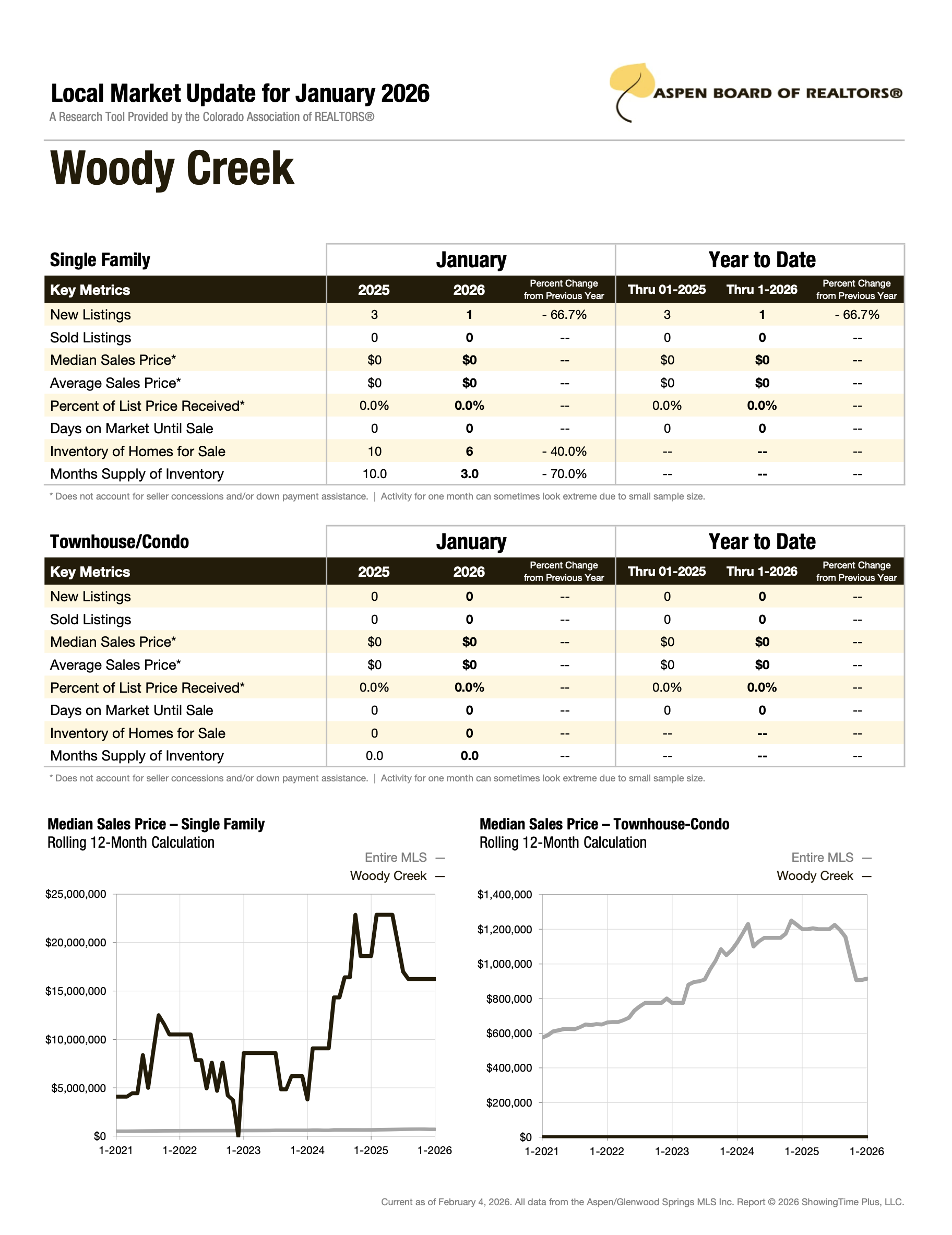

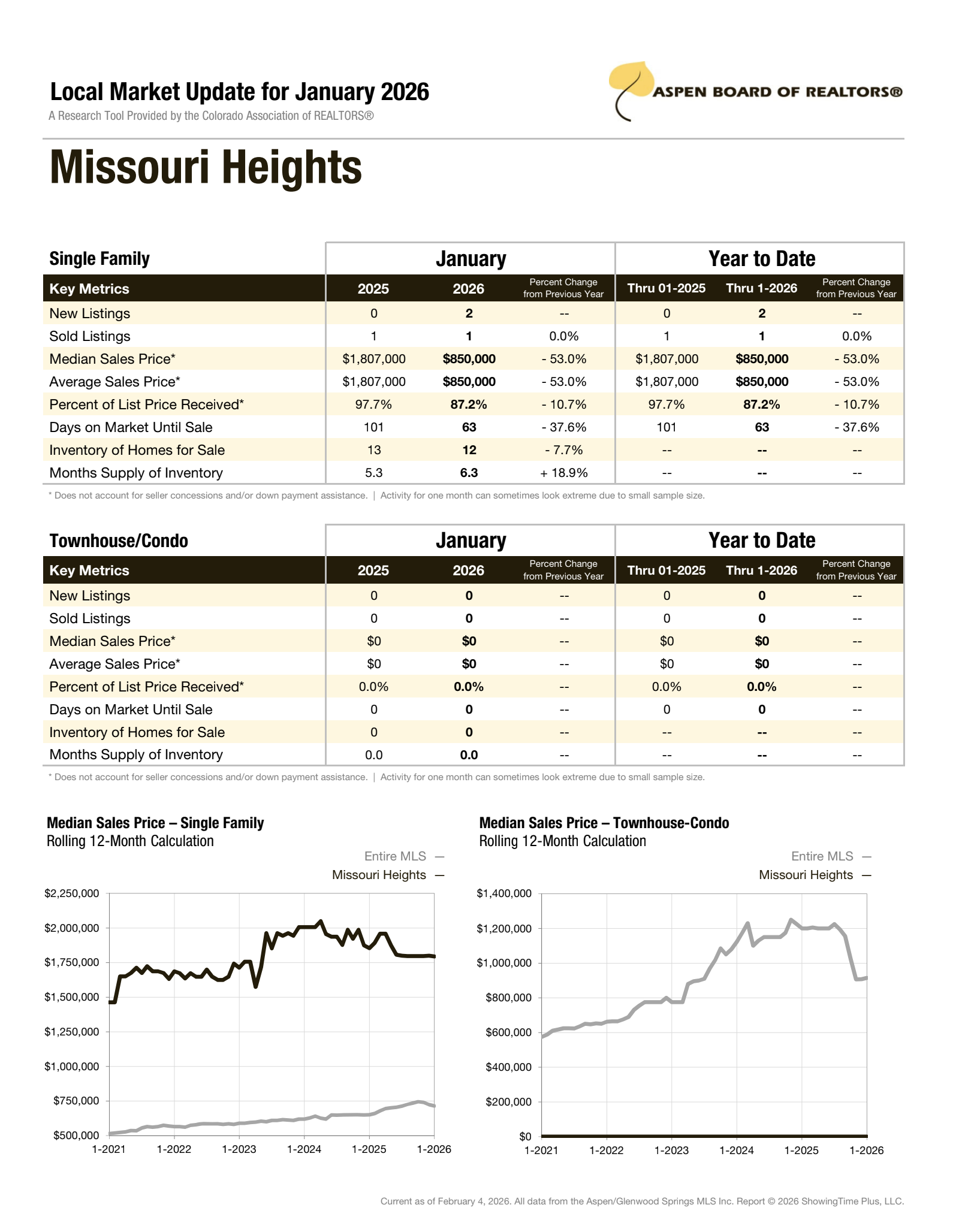

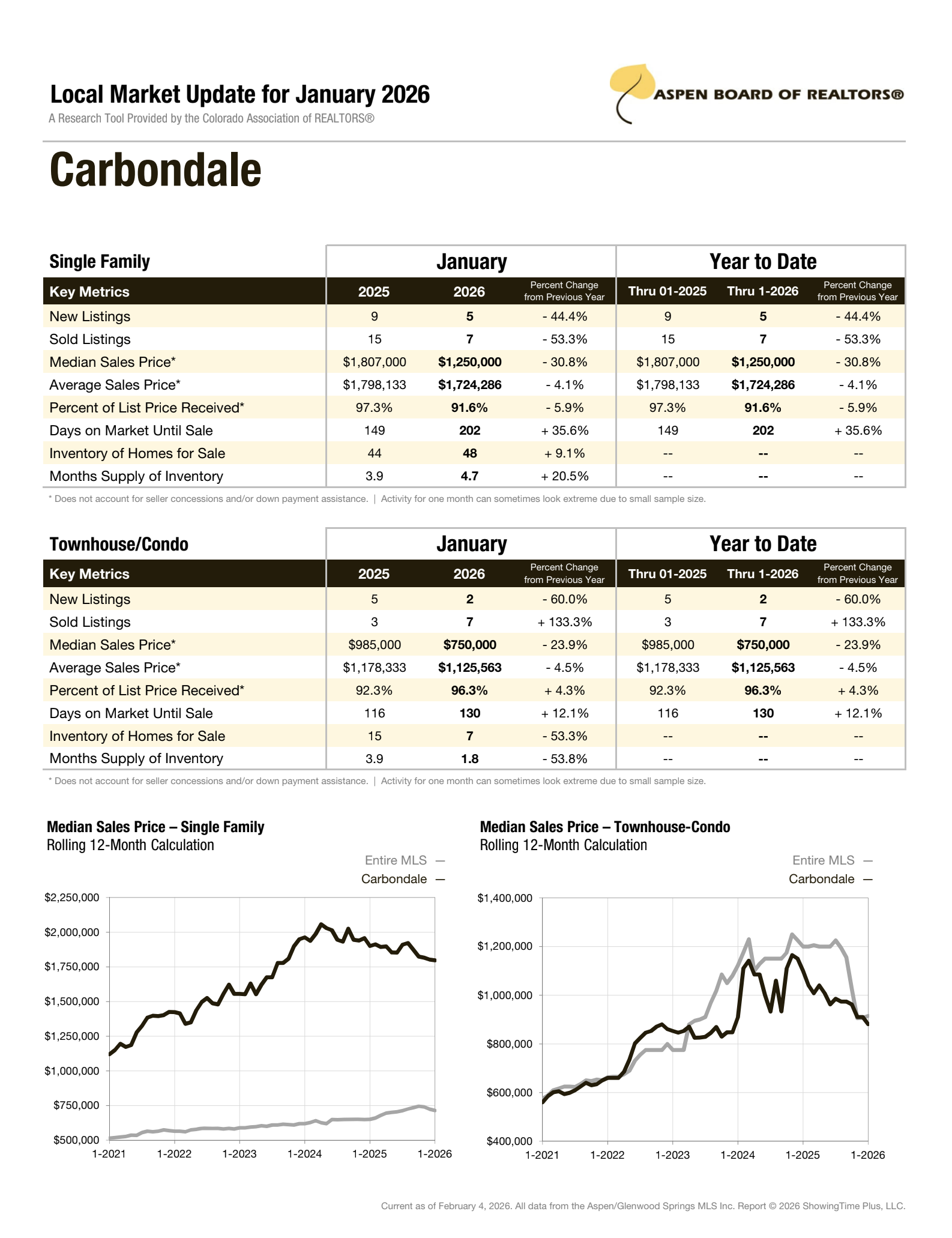

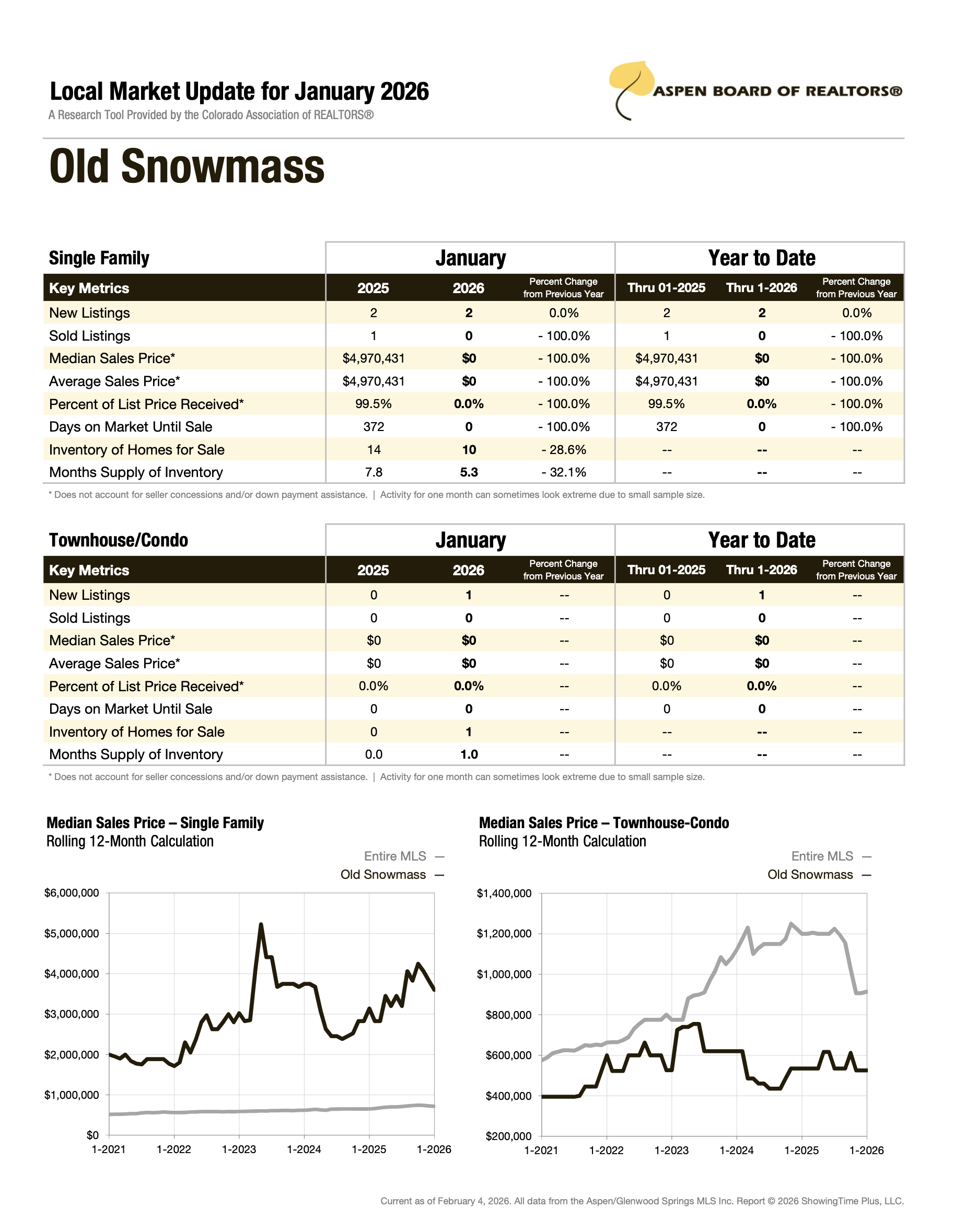

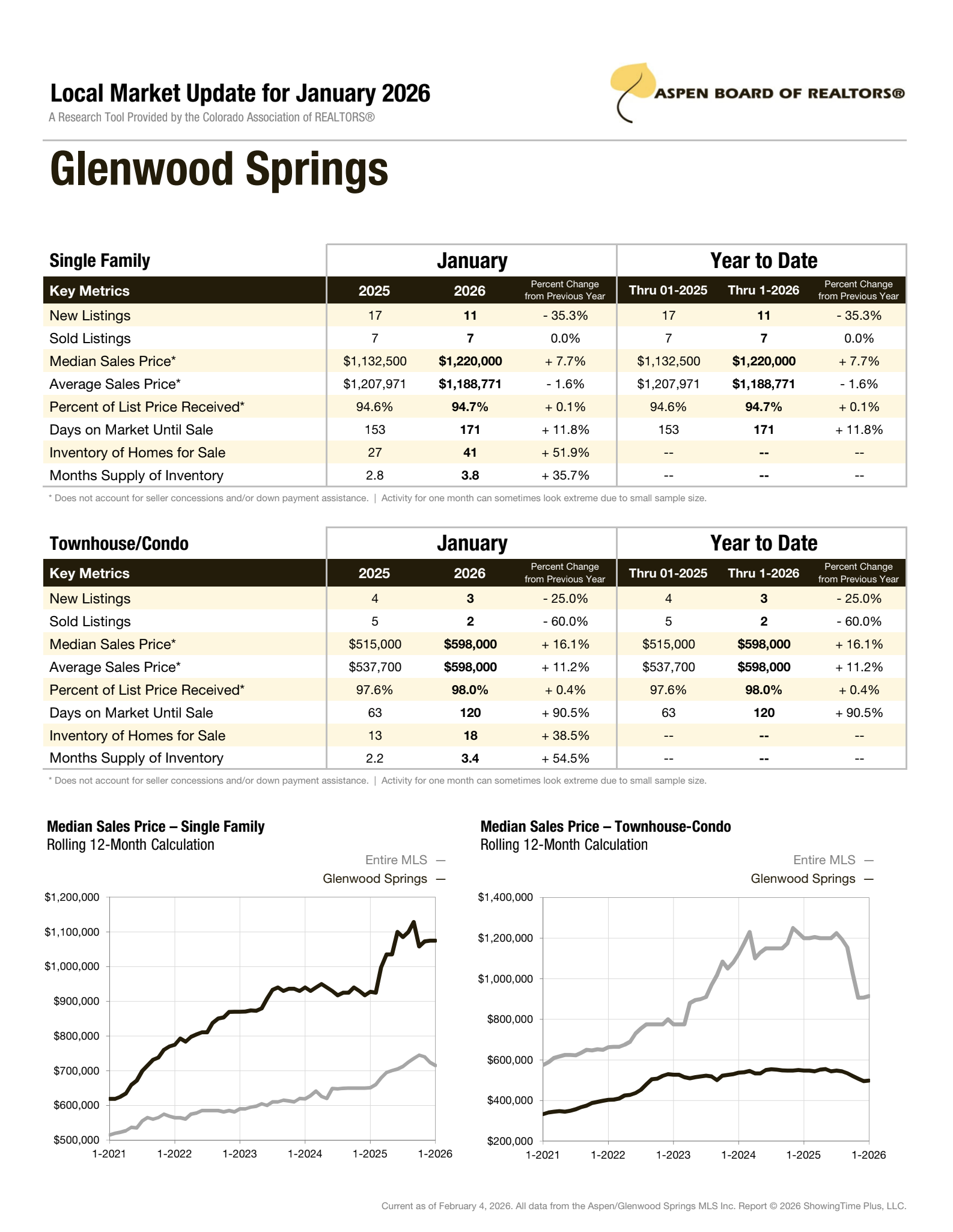

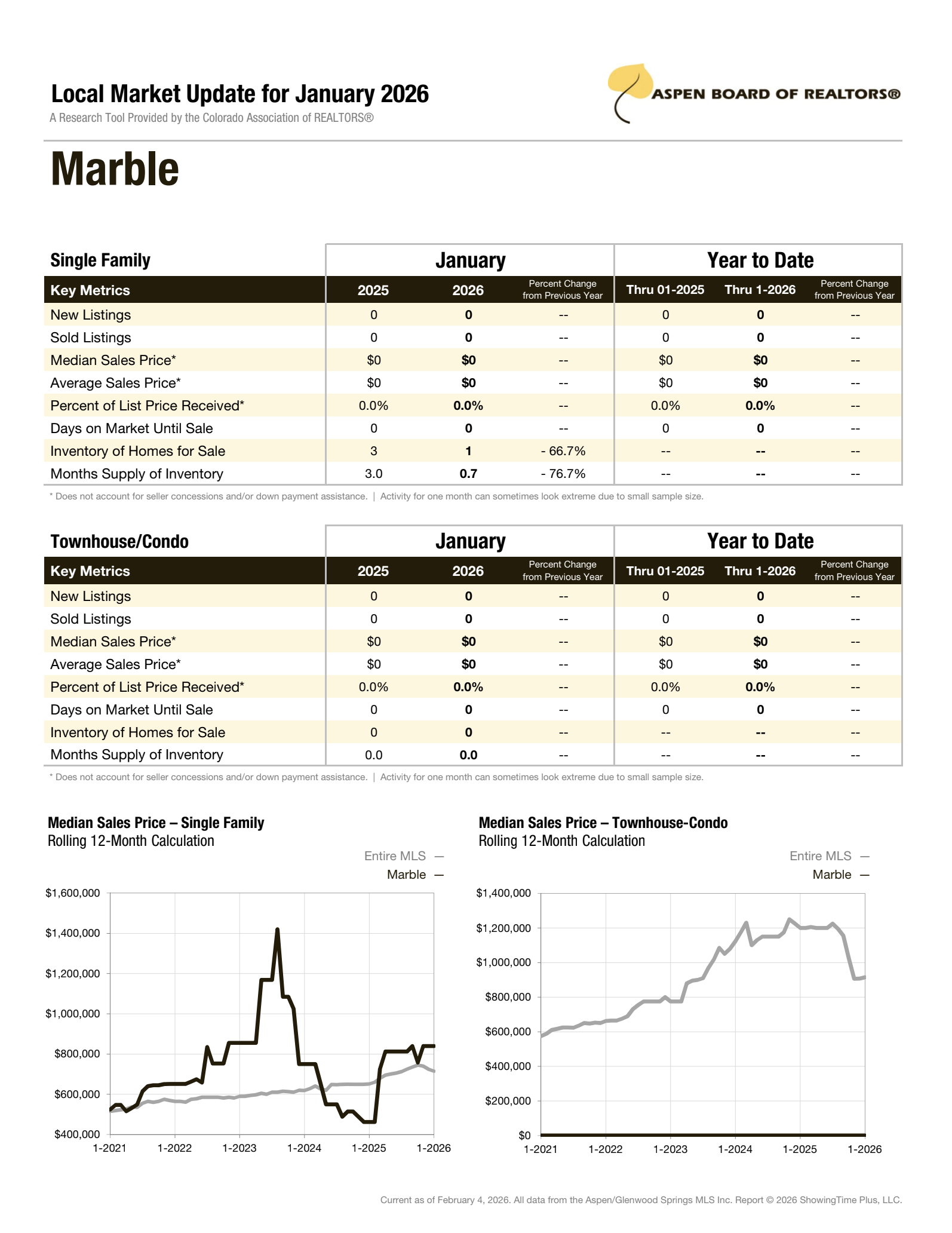

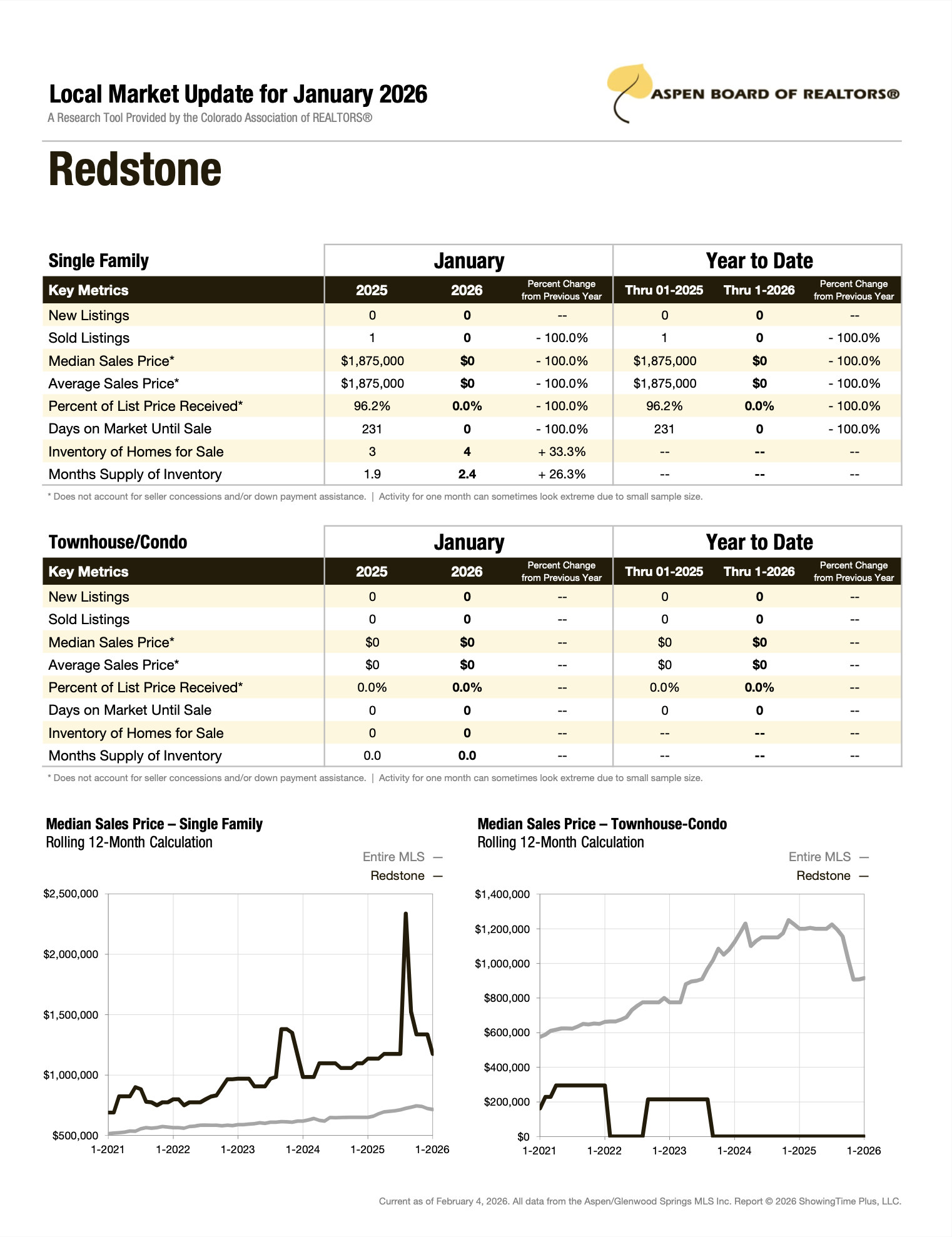

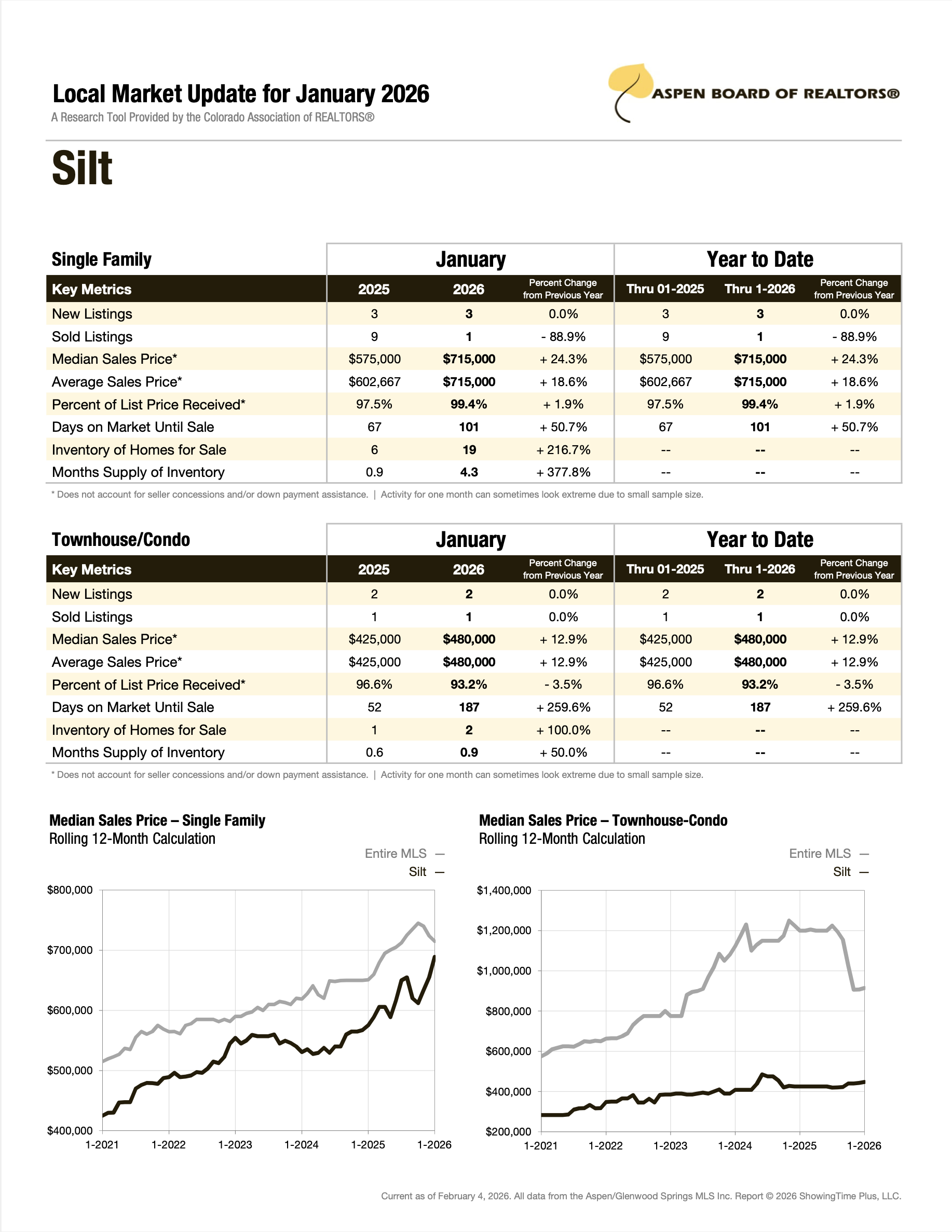

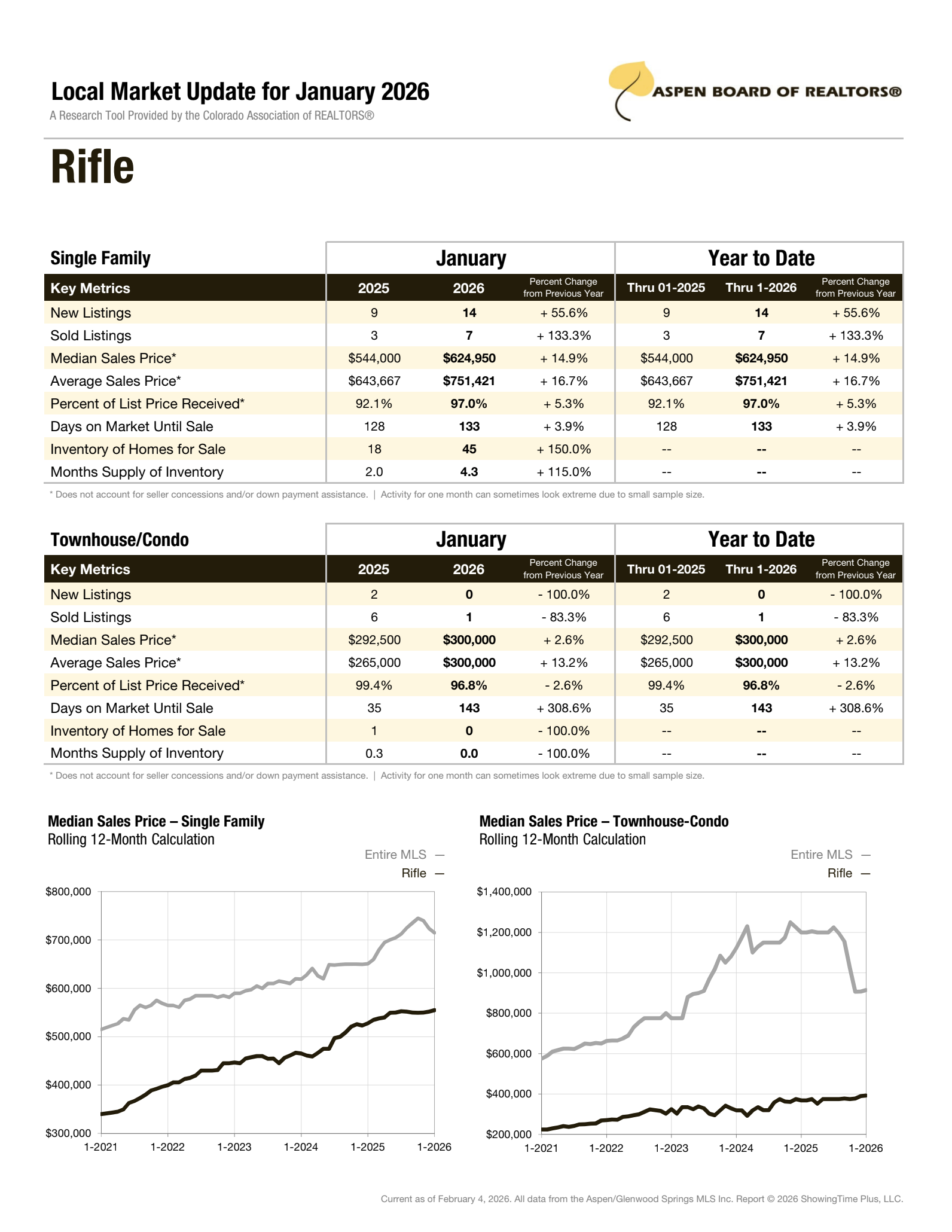

Strickingly, new listings were down 30% compared to the same month last year, with several areas having none at all (Missouri Heights, Redstone, Marble, had 0 new listings in January). The low inventory is the story of early 2026.

Let’s organize our local real estate in separate buckets, and analyze the trajectory of each category.

Luxury homes

In the luxury home sector, I’m expecting sales volume to be extremely low and most owners deciding to stay put because of the uncertainty and the stock market situation described above. Some might try to benefit from high valuations to sell to free up some cash and take that gamble, but it should be fairly marginal.

Second homes

There are a lot of second homes in the valley. These are actually used by their owner for their own enjoyment (unlike the third forth of fifth homes, in which cases they would fall into the luxury home category in the way people make decisions about selling them) and the current market shouldn’t entice people to sell them more than the usual. These are usually sold when life events happen, not based on market conditions so much. It’ll remain a pretty muted year in that category, most years are pretty uneventful in that section of the market anyway. That being said, a lot of economist tell us to keep an eye on the second home market, as the “silver Tsunami” approaches. As the wealthiest generation in human history transitions to the after life, a lot of analysts see the sale to transitions of their assets into the hands of the heir as a major factor that will shape asset valuations and trading. But that’s down the road (thankfully for those owners!!) and we wish them to prolong their ownership for as long as possible!

Full time resident and local worker homes

As we all know, the forgotten men and women of this valley are the working families that have to compete will all the above to put a roof over their heads. Things are not looking like they’ll get any easier for them to access housing this year. That being said, we also benefit from an exceptionally robust employment market. If you are one of our beloved working families in this valley, my only recommendation would be to hop on the bandwagon as soon as you can find yourself in a situation where you can afford homeownership. I truly believe that waiting on the sideline is basically digging your hole in the market we are in. Rents are high and getting higher, and as I described in the article I don’t see how home values can go down significantly in our valley in the dear future. Remember that the same forces to try to keep you out of homeownership will play in your favor once you own a home. Play the long game: Purchase a home that you can hold onto on the long run, and watch it go up in value over one, two decades. Set reserves so you don’t have to sell it in case of hardship. Find a home at a good location that needs work. Play the fundamentals. Nobody will be playing trading games with real estate in the near future, and it’s a great time to buy and hold strategy.

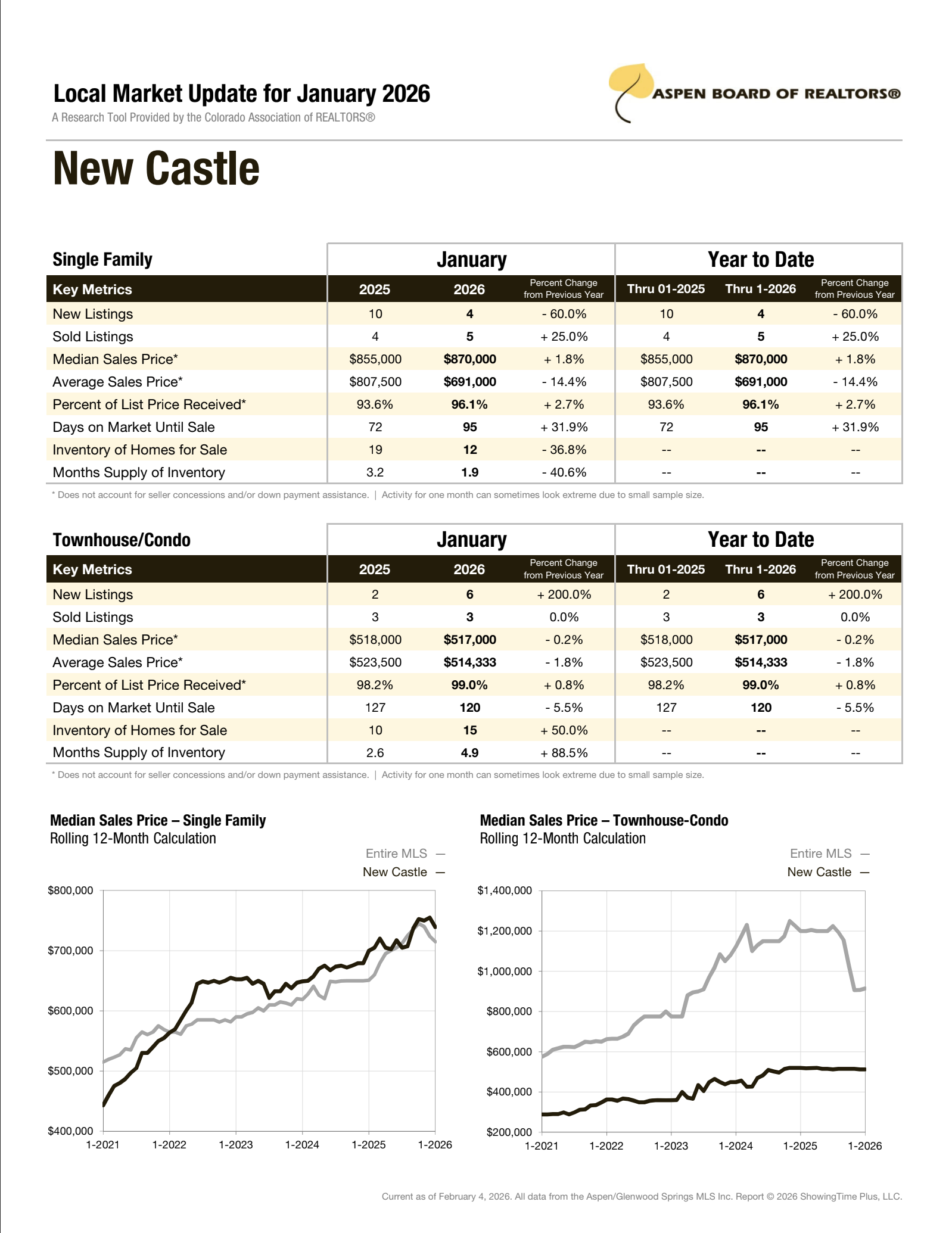

The latest statistical report for New Castle shows how slow we can expect this year in that section of the market. New Castle became the number one town for local working families, and it’s striking to see that only 4 homes were listed in New Castle in January.

STRs

This is difficult year for short term rentals. Nightly rates and occupancy have been slowing down and the weather has been playing against us with one of the worst winter snowpack in recorded history. Glenwood has been doing better than other towns thanks to the Hot Springs, where other towns rely heavily on skiing. The Aspen Times recently reported an almost 10% drop in occupancy in December compared to last year. I’m not expecting too much blood in the water there, especially if owner have been running their STR for at least a few years. Recently purchased ones with high interest rates might have a harder time. I’m also expecting interest in purchasing STRs to be fairly slow this year. That being said, that market overlaps with the second home market with owners wanting to both rent it and use it for themself when they want to, which maintains a certain level of interest.